Water into wine – the state of the industry considered yet again

By Christian Eedes, 24 January 2019

-

Share:

1

Is the South African national vineyard fit for purpose? With Chenin Blanc and Colombard making up approximately 20% of plantings and 40% of crop, the argument could easily be made that our varietal mix is not aligned with a world that wants to drink Sauvignon Blanc, Chardonnay, Cabernet Sauvignon and Merlot.

Conversely, if more than 80% of wine producers are not properly profitable as is often quoted, then why are there not more “For sale” signs dotted across the winelands? Perhaps it’s because that while the price per litre that wine gets sold for is a matter or record, cost of production is less easily determined and often gets overstated. “’n Boer maak ‘n plan” (a farmer makes a plan) as the saying goes…

At the recent Information Day held by the non-profit company representing local growers and cellars that is VinPro, chairman Anton Smuts made the provocative point that “14% of our bulk white wine sells for under R4.50 while water sells between R5.00 and R6.00.” Not an ideal situation when you consider that it takes 500 litres and up to make a litre of wine.

Then again, probably not that useful to conflate what is happening at the bottom of the market with what’s happening at the top. As Christo Conradie of Vinpro management observed, “You average 10 and 90, you get 50,” his point being that we should be careful about sweeping statements about the state of the industry.

Robert Joseph, former fine wine writer and now brand consultant and producer, argued that when it came to packaged wine, it was the stuff premised on being an expression of “terroir” that attracted all the media attention but there were nevertheless a number of other more or less viable categories – wine as Liquid Luxury Good, as Issue Driven Purchase, as Fashion Driven Purchase, as Curiosity Driven Purchase, and wine Bought Like Perfume. Perhaps the most pertinent slide of all in his presentation was that it was beholden on producers to “transcend category” and here he referenced Cloudy Bay Sauvignon Blanc out of New Zealand in particular…

The challenge for so many producers, however, remains a vicious circle where a low selling price results in a low margin, no marketing budget and a weak brand. In this regard, it is staggering that just 11% of still wine sold for over R72 a bottle in the period January to October 2018 while 49% sold for under R30.

While the bulk wine, commodity wine and fine wine sectors all have significantly different market dynamics, they are, at the end of the day, inter-related. Price per litre has to go up across the board and the national vineyard will continue to decrease (down from 101 957ha in 2007 to 95 545ha in 2017) until such time as demand and supply are brought into equilibrium in the most basic terms. We must hope that while this process plays itself out, we don’t lose any old vineyard that might be capable of making the next Ou Wingerdreeks Skurfberg or Alheit Magnetic North…

Not a pretty picture.

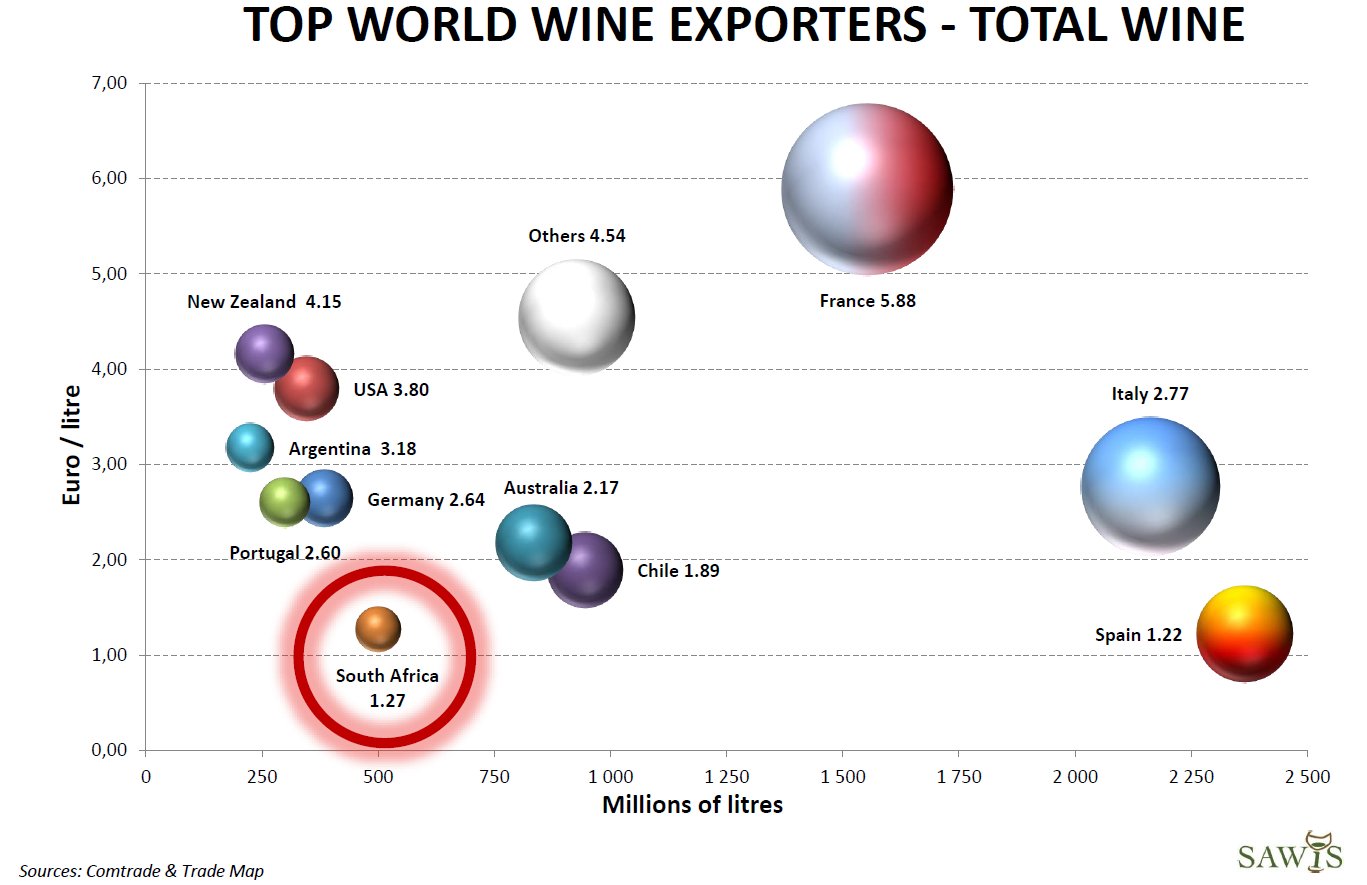

The other concern, of course, is that with the structure of the South African wine industry such that we sell 60% of our wine in bulk, we look like the also-rans in the world of wine. Agricultural economist Wandile Sihlobo showed a slide that South Africa has an average price of 1,27 Euro/litre for total wine exported, the second lowest after Spain with 1,22 – the latter having vastly more hectares under vineyard. This situation obviously does nothing to help how SA wine is perceived as a brand in an overarching sense.

-

Share:

David Clarke | 24 January 2019

Nice read, Christian. A lot to ponder.