Greg Sherwood MW: The Great Wealth Transfer and the coming fine wine market reckoning

By Greg Sherwood, 26 March 2025

-

Share:

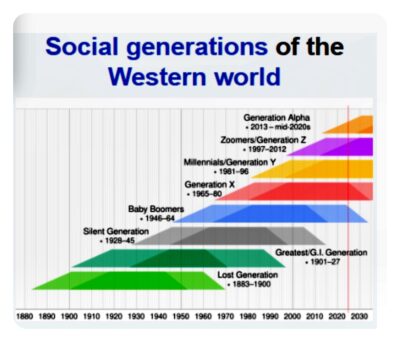

The Great Wealth Transfer refers to an intergenerational wealth transfer that is currently underway in the United States as well as among many other western nations, with the Baby Boomer generation (born 1946-1964) leaving significant wealth to their heirs. Baby Boomers and the Silent Generation (born 1928-1945) together will bequeath a total of US$84.4 trillion in assets through to 2045, with US$72.6 trillion going directly to heirs. The transfer of wealth from Baby Boomers will account for US$53 trillion, or 63% of all transfers, while the Silent Generation will hand down a tidy US$15.8 trillion, according to Andrew Lisa’s book “The Great Wealth Transfer: How Baby Boomers Are Passing on Trillions to Heirs“.

Inheritance has become increasingly common among U.S. households, with 60% surveyed in 2022 having received, expected to receive, or planned to leave an inheritance. Wealthy individuals make up only 1.5% of all households but constitute 42% of the expected transfers through to 2045, or approximately US$35.8 trillion. The wealthiest 10% of households will give and receive the vast majority of this wealth, with the top 1% left holding about as much real wealth as the entire bottom 90%.

Of course, this transfer of wealth is influenced by many factors such as price growth in real estate and financial assets, housing discrimination based on where you live, and the general lack of access to financial services for many people of colour. The US tax code in particular, which allows individuals to transmit large sums without federal estate tax, contributes to the enormous scale of this impending transfer.

But what of the unintended consequences of this great wealth transfer? What will the wider impact be on the greater economy, the availability and pricing of housing stocks, on education standards, healthcare costs, as well as the general financial markets and labour markets? What seismic changes can we expect once this wealth transfer is well and truly underway and how may it affect sectors such as the wider fine wine market?

While many of the above figures bandied around are specific to the USA and clearly serve to illustrate the scale, similar transfers are envisaged and are already being observed in the UK and across the wider European continent. With such large sums of money involved, it is not only innovative businesses that are examining potential opportunities to tap into this migrating wealth pool, cash-strapped national governments are scrambling to find ways to increase their share of inheritance tax and the broader transfer of generational wealth.

What does this all have to do with the fine wine market you might well ask? Quite a lot, actually! Only last week, I engaged in a very interesting chat with industry stalwart Simon Farr, the 2013 co-founder and chairman of Cru World Wines, who with investment from a European investment firm, initially acquired two existing businesses with great teams and fine wine allocations, and which today form the foundations of his company Cru, specialising in high-end blue-chip Bordeaux and Burgundy.

Simon is himself a Boomer, and at 71 years old, he said he was witnessing first-hand the beginning of this great wealth and asset transfer. But more importantly, this specific demographic group was also the golden generation who magically had both access and the means to buy large quantities of international fine wine stocks at prices that would seem simply alien in today’s inflated market.

Quite simply, this is the same generation that in the UK alone, is estimated to be sitting on approximately £5 to £6 billion pounds worth of fine wine in underbond storage, professionally stored in one or another of His Majesty’s Revenue and Customs (HMRC) controlled bonded warehouses, where duty and VAT are only payable on the original historical cost of the wine when the physical stock is removed from storage for delivery to the client.

As one of the world’s leading fine wine trading capitals, it comes as no surprise to me to hear of the sheer volumes of fine wine in storage across the UK. However, Simon then pointed out that the accumulative storage bill for all these wines annually was also inflating, reaching staggering levels of cost. With more and more of these wines now classified as blue-chip assets costing hundreds or thousands of pounds per bottle, stocks are not being consumed on the scale and at the rate in which the fine wine market ideally requires them to be.

There is a veritable glut of fine wine in storage, being financed and paid for by successful affluent Boomers, who on the whole, are actively seeking to drink less for health reasons or have given up drinking altogether on medical advice. So, the fine wine market has become more and more constipated, with the potential solution – the eager drinking Generation X’ers and Millennials – are often unable to afford these wines anymore, as they buckle under stagnating private sector salaries, continuous tax rises, high mortgage rates, soaring private school fees, and a general cost of living crisis that has ensured that even the most affluent of these next generations of drinkers are having to tighten their belts and cut their fine wine purchases.

Quite clearly, much of this fine wine will by necessity, eventually be circulated back into the wider fine wine market and put up for sale, and in Simon’s opinion, will create a temporary oversupply scenario that could easily result in price suppression for the coming five or more years. Alternatively, even if many of these asset-class fine wines are merely bequeathed to the next generation for free, the headache of the sizable storage bill will still need to be financed by somebody.

While some individuals will clearly benefit from the great wealth transfer, others will face dual challenges, such as the ‘sandwich generation’ dealing with the rising cost of caring for ageing parents who are living longer and children unable to leave home simultaneously.

The self-financing gap remains a big concern, with many workers, specifically Generation X’ers facing insufficient retirement savings and being financially unprepared to retire. Simply put, these disparities do not bode well for discretional spending and the fine wine market in the medium term.

- Greg Sherwood was born in Pretoria, South Africa, and as the son of a career diplomat, spent his first 21 years traveling the globe with his parents. With a Business Management and Marketing degree from Webster University, St. Louis, Missouri, USA, Sherwood began his working career as a commodity trader. In 2000, he decided to make more of a long-held interest in wine taking a position at Handford Wines in South Kensington, London, working his way up to the position of Senior Wine Buyer over 22 years. Sherwood currently consults to a number of top fine wine merchants in London while always keeping one eye firmly on the South African wine industry. He qualified as the 303rd Master of Wine in 2007.

-

Share:

Related articles

Opinion & Analysis

Greg Sherwood MW: IWSC Top 50 – SA up, France down

19 November 2025

As we approach the end of another eventful year in wine, the written contributions from both Winemag’s columnists and editor seem to get ever more philosophical and reflective. Christian Eedes’...

Opinion & Analysis

Greg Sherwood MW: Sadie’s ‘T Voetpad and the power of old vines

6 November 2025

The Western Cape winelands have been blessed with a rich tapestry of viticultural diversity, sometimes by design, sometimes by default and sheer luck. Take the 5,159 hectares of old vines, defined...

6

Opinion & Analysis

Greg Sherwood MW: Shifts in the Southern Rhône and what SA wine can learn

8 October 2025

It’s sometimes funny to think that wine producers, regional bodies, and certainly consumers in South Africa so often look to the classical Old-World regions of France, Germany, Spain, and Italy...

Comments

0 comment(s)

Please read our Comments Policy here.