Michael Fridjhon: Bordeaux’s bubble bursts – and lessons for Cape wine

By Michael Fridjhon, 13 May 2026

-

Share:

15

An interesting corollary of the general decline in wine sales worldwide has been the collapse of the wine investment market. This is not something immediately evident to the average South African fine wine drinker, However, if you were living in the UK and had been buying Bordeaux En Primeur for many years (ostensibly for your pleasure, but often because you were told it was a great investment and a useful component of your retirement portfolio) you would be acutely aware of the situation.

The Bordeaux wine trade has long depended on the concept of En Primeur sales – which work like this: a percentage of the latest vintage is offered for sale by the chateaux through the Place de Bordeaux. Typically the campaign begins in the April after the vintage. The incentive for the buyers is that the earliest price would (in theory) be the lowest: in the heyday of demand the chateaux would release several “tranches” over a few weeks or months with the price for each succeeding parcel higher than the one before. Buy early, buy cheaper is the message. Built into the idea is the expectation that as the wine ages and gets better, bottles are consumed, so that rarity increases alongside its enjoyment potential – so that a growing shortage coupled with added pleasure would drive the prices upwards.

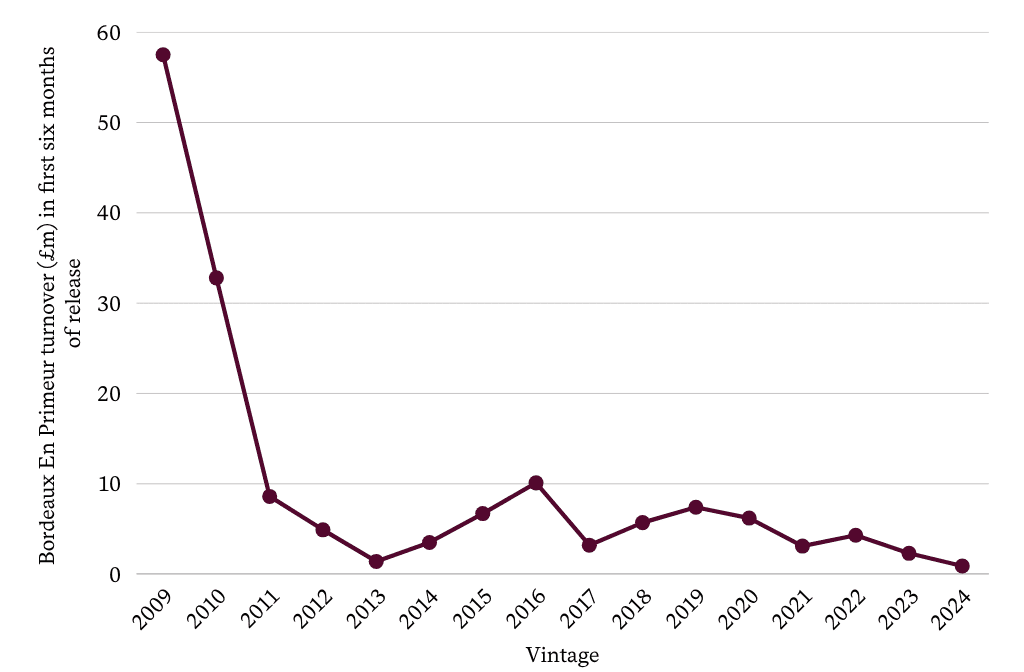

This model has worked well enough – certainly from the 1980s and until late late 2010s (so, depending on whose hymn-sheet is being held up to scrutiny, probably 2018/9). But for much of the past two decades most of what Bordeaux was offering for sale at increasingly elevated prices was acquired for investment not consumption. The pipeline was filling, there was little or no off-take, and buyers were beginning to discover that they could not sell their purchases for the anticipated profit. Anyone who did the arithmetic properly soon worked out that the opportunity cost involved in tying up money in stock, plus the actual costs of storage etc, could not be covered by the prices buyers were prepared to pay. So by 2025, when the 2024 vintage came to the market, there was simply no demand while the prices in the pipeline kept on falling.

The numbers are instructive: Farr Vintners sold £60m of the 2009 primeurs and less than £2m of the 2024s. No one was buying the Koolaid. Meantime, based on average purchase prices, several of Bordeaux’s best vintages were under water – even before taking into account holding and storage costs: for example, 2009 was at -7%, 2010 (an even better year) was at -19%, while more current releases were no better: 2016 is at -11%, 2018 at -26% and 2020 at -29%. There are a lot of people talking up the prospects for the about-to-be released 2025s (a small but seemingly very good vintage) but the truth is that the game is up.

The reason for this is not because – as Greg Sherwood MW has asserted in these pages – technology has provided data-transparency where previously trader “expertise” called the shots. It’s much simpler than that: the size of the problem was too large to conceal any longer. The negociants who are the middlemen in the en primeur universe have huge unsold inventory so they simply cannot continue to participate in the charade. Nor are their customers buying; the investors are not investing (they are trying desperately to unload their holdings without the whiff of panic permeating the trading floor). To quote Monty Python, prices are not so much flying as plummeting.

This is – and was always going to be – the endgame to a bubble. Forty years ago you could buy a decent classed growth Bordeaux for R15. You can apply any index you like for inflation and rand devaluation but you won’t get anywhere near the R3,000 per bottle the 2022 vintage of the same wine was supposed to be selling for. Growing demand pushed up prices but – and this is the nub of the problem – a huge chunk of that demand was not consumer driven, it was speculation.

What, you may ask, is the relevance of this looming crisis in the Bordeaux trade to the Cape fine wine business? The answer is a great deal: wine investment has been touted by a number of players in the industry. Their message has often been framed using the indices of big name Bordeaux, essentially suggesting that the same returns which were achieved between 1990 and 2020 by the European fine wine funds are possible here.

So far many appear to be right – but this is because the trade is so thin that the results can be manipulated. The head of an auction house which has made a name for itself recycling collectible Cape wine once admitted to me that the only reason the prices look so good is that the volumes are very small and so demand (for the moment) exceeds supply. To paraphrase his comment “if there were ten cases instead of six bottles of any of the trophy wines on our sales, the prices would fall through the floor.”

It’s not too late to learn a lesson from the catastrophe unfolding in one of the oldest and best respected wine producing regions in the world. It starts by remembering that wine is not a commodity to be traded but a beverage to be enjoyed between friends.

- Michael Fridjhon has over thirty-five years’ experience in the liquor industry. He is the founder of Winewizard.co.za and holds various positions including Visiting Professor of Wine Business at the University of Cape Town; founder and director of WineX – the largest consumer wine show in the Southern Hemisphere and chairman of The Trophy Wine Show.

-

Share:

Related articles

Opinion & Analysis

Michael Fridjhon: Fine wine fame is earned one visitor at a time

15 July 2026

Many South African wine producers, especially those who are relatively recent arrivals on the international stage, lament the years of isolation – not just the 1980s as an era, but...

3

Opinion & Analysis

Michael Fridjhon: The Tim Atkin Special Report and the question of independence

10 June 2026

The news, announced recently by Wines of South Africa (WOSA) to its members, that henceforth producers would have to pay to have their wines rated by Tim Atkin MW for...

56

Opinion & Analysis

Michael Fridjhon: When the media dies, fine wine becomes just another lab-grown luxury

15 April 2026

We are one of the world’s top ten wine-producing nations. We have what is arguably the most creative and exciting wine industry on the planet – and yet we cannot...

Jamie Johnson | 13 May 2026

Totally agree and in SA there aren’t many wines that I’ve seen personally make sense to hold for investment purposes when taking into account storage, inflation etc. Those that are, I prefer to drink myself (Sadie, Alheit). It’s only the 100pt TA wines that seem to go crazy on the secondary local market for some reason (which doesn’t happen internationally).

keith | 13 May 2026

100% agree Michael and my BBR cellar valuation over the last 20 years of buying EP , has plummeted in line with your graph. Of course, the upshot of this is that my friends and relatives are now much more likely to benefit than my bank account !!

Regards

Keith

Greg Sherwood MW | 13 May 2026

My article on AI and tech pricing transparency merely identified the latest complication and an additional reason why wine investment has become harder if not impossible for Bordeaux. The root causes of a declining wine investment market are of course multiple, none more so than too much supply and not enough demand… and of course unsustainably high release prices.

Bruce Ellison | 14 May 2026

Thanks Michael. It’s a good article and appreciate the facts to sum up the context. Truth is, there’s a lot of Bordeaux made – and it had reached rather silly and unaffordable prices, as u say, driven by speculation. The best is still eyewatering expensive, so perhaps we have just seen a return of prices to common sense. I’d bet these estates are still making money.

For SA wine – yes there will be some impact – as upper price points sd now be more limited. I see friends rightly questioning prices of “me too” offerings of old vine Chenin, and the “luxury” SA Bdx editions. The big estates generally can’t charge huge prices and sell large quantities of stock – so this has been where good value has been found in SA. The Sadie and Alheit’s, if they can maintain quality and brand presence- I’d suggest is more of a Burgundian model of scarcity and brand -with pricing supported by customers who want to try the best. I’m not sure we see these prices fall – in fact if joburg has a resurgence I can see these wines becoming rare and sought after trophies- with price hikes to match. Especially as a lot of these wines are drunk on release – because most people don’t have storage, and if you only get one or two bottles ur curiosity is too great to try one. Im not sure anyone has spare stock of these wines – so, they may truly be “collectible” as they sd demand time in the cellar too.

I don’t see or expect any premium $ upside on keeping my SA wines in the cellar – other than the joy of drinking them when they are ready. And I’ve not seen any real upside in 30 years of being here. There sd be a market for mature and well kept SA wine- as it’s a good product – but I’m not sure it’s ever been an economic one.

SJB | 14 May 2026

There have been a few articles recently on winemag about the demise of the en-primeur system in Bordeaux and the fact that older vintages are trading at discounts to current releases.

What does this mean anything for the SA-based consumer? Are these older ‘discounted’ vintages making their way into our market at all or is the market too small and controlled by a few large merchants for this to happen? Or is this just of academic interest to winemag subscribers?

Michael Fridjhon | 16 May 2026

The short answer is that prices are easing. Obviously there’s stock in the pipeline so importers are trying to salvage margin in a bad situation. The smart ones are offering decent discounts and keeping their powder dry so that they can go shopping in due course. There will be bargains if the Rand holds and prices don’t bounce back: Cru Classe wines from decent vintages for R1200 per bottle

SJB | 18 May 2026

Thank you Michael. An opportunity for a few follow up articles to flag some of these wines to local buyers as they become avaliable. With the prices of top local Bordeaux blends now more regularly approaching or breaching R1000 a bottle (Paul Sauer, Lady May, etc.) It’s no longer necessarily obvious that the local pick is always better value.

Roland Peens | 15 May 2026

Hi Michael

I am surprised by your comment ‘because the trade is so thin that the results can be manipulated’. From a Strauss & Co point of view, we are short stock on many auctions. The demand for fine wine has grown along with the supply. How could it be manipulated?

We backed South African wine as worthy of cellaring, and trading when necessary. Thank goodness we did, otherwise we would still not have a secondary market for South African wines – a requirement of a fine wine market.

And prices have fallen since the 2022 international peak. Great, a functioning market. But very often the South African returns are still higher than the touted returns you mention.

GillesP | 15 May 2026

I agree with Roland here. Anyone who follows closely the Strauss auctions results can attest to that.

Michael Fridjhon | 15 May 2026

Hi Roland

I wasn’t surprised when I read your comment: Strauss has done a fine job of creating and sustaining a small secondary market in South Africa. It works for a few wines and a few – generally quite hard to get – brands. But it’s hardly a market in which the speculators can move in and out with ease, or with volumes big enough to make wine a genuine alternative asset class.

After one of your very first auctions – when a 1986 Vin de Constance (the launch vintage, so rare, but not by any means the best) – sold for around R25k I contacted you because a few of my friends thought it would be the right time to sell. You said you wouldn’t be in a position to consider any stock until a least the next year. I’m traveling at present but I’m sure I could find that exchange if you needed me to. I’d call that a thin trade.

Then there’s the question of whether the market could sustain tradeable volumes of the high-profile rarities. Thousands of cases of First growths pass in and out of the secondary markets of London and HK every year. I think you would have to agree that you couldn’t take 100 cases of Columella – probably the rarest of the high profile SA wines – without an impact on the auction prices. Your chairman said as much to me a few years ago.

Finally, now that we’re on the subject, there’s the small question of the auction commission – seller’s and buyer’s. If you were really committed to a true secondary market there wouldn’t be an in/out cost of over 30%. Stocks trade on tiny percentages: wine investors lose a significant chunk of the gains they have made through prescience and time the moment their wines go on auction.

This doesn’t mean that you’re not delivering a service: people can tidy up their cellars, dispose of wines they’ve fallen out of love with, and find wines they weren’t foresightful enough to buy in the first place. But you’re offering a luxury trading platform for (largely) luxury goods – not an exchange for wine investors

GillesP | 15 May 2026

Thanks for calling up the outrageous level of commission from Strauss . In the UK people selling high end Malts in Auctions are at 5%

30% with Strauss in and out! Shocking.

Wessel Strydom | 16 May 2026

I am sure the prospective seller and buyer are aware of the commission percentage at Strauss. Should they decide to continue with the transaction then surely all is fine. The old adage of willing buyers and willing sellers..

GillesP | 16 May 2026

Of course they are aware. Doesn’t stop the fact that these commissions % are too high and not on par with other international auction houses.

YEGAS Naidoo | 16 May 2026

Very interesting dialogue on a meaningful current day concern with long term wine investors – speculative or not. Michael, I wonder what your take would be on current day astronomical auction / secondary trading prices on Hermes Birkin and Kelly handbags. A strong web has been knit with pricing on these luxury accessories.

Michael Fridjhon | 16 May 2026

Hi Yegas

It’s flattering you think I have any special insights on the high-end fashion sector. I have been following some of the extraordinary Hermes trades on Christie’s and Sotheby’s. Here the really high-priced items have come with impeccable provenance and real history. There are always people with enough money to pay vastly more than the functional value of an object but they generally want what no one else can get. That was what was so appealing about Jane Birkin’s prototype HAC bag sold late last year.

Many of the other trades are driven by impatience (not wanting to wait a few years for delivery) and by the certainty that the object in question is genuine rare and that ownership conveys wealth. Isn’t that what some people actually buy Petrus and Romanee-Conti for?